FEDERAL GOVERNMENT FACILITATES THEFT ON A GRAND, SYSTEMIC SCALE

by Steven Neill, ©2013

(Feb. 25, 2013) — Almost daily Americans are treated to a new set of sound bites as the last set wears thin. From Romney’s “47%” comment to these headlines “Republican Party in Disarray;” “Hurricane Sandy, Storm of the Century;” “Sandy Hook;” and “Fiscal Cliff,” we are inundated with sensational stories meant to distract, marginalize, push an agenda and keep us from looking behind the veil. One has to wonder if as many Americans would still be asleep if instead of nonsense headlines like Romney’s “47%” statement the media were to print the almost weekly bank scandals? Maybe the media could publish articles on how much money these “too-big-to-fail” banks give in campaign contributions and to which politicians they give it; that might raise the circulation a bit. Why is it that these stories appear for one day then are relegated to page 6 under a cell phone advertisement, then gone completely? This situation is certainly not unlike the ill-fated Sultana disaster of 1865, where government corruption, company greed and wrongdoing were ignored by a media bent on prioritizing the news that Americans received. Only this time it’s on a much bigger scale.

Room for One More

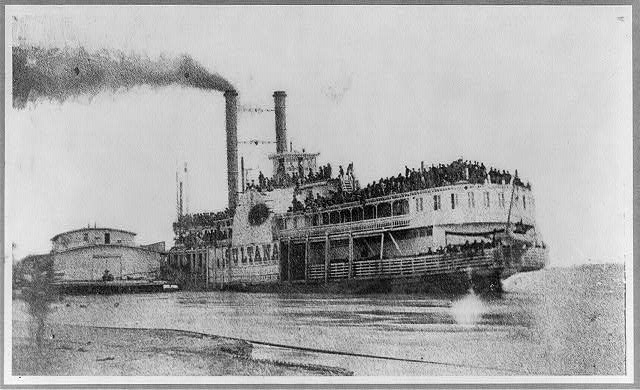

Launched in January 1863, the side-wheeled steamer was named Sultana, which meant a sultan’s wife, sister, or mother and was an extremely popular boat for river travel and transportation during the war. It measured 260 feet in length and had the capacity to carry 1,000 tons while trimming only 34 inches of water, thus making it ideal for travel on the Mississippi, Ohio, and Tennessee rivers. It provided accommodations for 376 passengers including crew, which was the Sultana’s legal capacity. During the war, it served the North well by transporting men, supplies and munitions all over the river systems. [1]

In the closing days of the American Civil War, riverboats were being paid to transport the newly-freed Union prisoners from Andersonville prison camp in Georgia to Cairo, Illinois for release from the Army. The Federal government was paying $5.00 per soldier and $10.00 per officer to get these men home, which at the time was huge money. As with most government programs, it was rife with corruption as the officials in charge of sending the men home demanded a $1.15 kickback from the ship owner to assign men to a particular ship. [2] Sultana Captain J. Cass Mason (who was also one of the ship’s owners) was desperate to get his share of the Federal payout, but on April 21, one of the boilers developed a leak and had to be repaired. The boilermaker, R.G. Taylor, told Captain Mason that two sheets on the boiler needed replacing. Concerned about time and money, Captain Mason refused and told Taylor to patch the boiler instead. Taylor disagreed with Mason but made the patch for the Sultana anyway.

Sultana arrived in Vicksburg on April 24th and found two other ships in front of it waiting for soldiers to take north. Captain Mason and other Sultana officers lobbied and bribed prison officials to let their steamboat take all the soldiers. The tactic worked. The Sultana left the dock on the evening of 24 April 1865 with approximately 2,100 troops, 200 civilians, and cargo, more than six times its legal carrying capacity. [1] [3]

Overburdened and poorly patched, Sultana struggled against a flooded river and made it seven miles north of Memphis, TN on April 27th. At approximately 2:00 am, a blast sent red-hot shrapnel and steam from the boilers to the decks above, killing or maiming scores of passengers instantly. The explosion hurled people into the air and out into the swollen, frigid river. Passengers threw doors, shutters, mattresses, bales of hay, and anything else buoyant overboard. [1] [3]

In their rush to get away, the terrified people trampled each other underfoot to escape the inferno on the boat. Many could not swim so they looked desperately for something that would float, but even then, many drowned in the turbulent water. At the start of the disaster, many passengers made a mad dash for Sultana’s lifeboat, and those who were lucky enough to get on board fought off their fellow passengers to keep from being pulled out of it. When boat lines were cut, the boat landed upside-down in the river, drowning most of its occupants. [1] [3]

The explosion had been heard in Memphis, some seven miles away, alerting people of some disaster downriver. Almost immediately, rescuers left the city, but they did not arrive to the actual site for almost two hours and by then, there was little to do but collect the dead and wounded from the riverbanks. Boats searched for survivors all morning but stopped looking by midday. Of the estimated 2,300 passengers, only 600 survived. The rest were killed in the explosion, drowned in the dangerous currents, or died soon after their rescue. [1] [3]

On 30 April 1865, Secretary of War Edwin Stanton created a board of inquiry to investigate the Sultana disaster. The board received testimony from surviving crew, passengers, and steamboat experts, but their reports only shifted blame from one person to another. Without conclusive evidence, the board decided that insufficient water in the boilers created the explosion and that overcrowding did not cause the catastrophe. No individual was blamed for the tragedy; no one was charged for so grossly overloading the Sultana, and none of the victims were compensated for their loss. [1] [3]

The Sultana tragedy remains America’s greatest maritime disaster, killing more people than those who perished aboard the HMS Titanic some 47 years later. Yet the tragic story remains largely forgotten in the wake of Lincoln’s assassination and the end of the Civil War. It should, however, serve as a sad testimony to how corrupt the government and corporations can be. [1] [3]

We Made a Mistake

In November 2012, HSBC, Europe’s biggest bank, agreed to pay a $1.92 billion fine to US authorities, settling a ten-year investigation into the bank’s money laundering for Mexican drug lords, terrorist organizations and rogue states. A report compiled for a US Senate committee detailed how HSBC subsidiaries transported billions of dollars of cash in armored vehicles, cleared suspicious travelers’ checks worth billions, and allowed Mexican drug lords to buy planes with money laundered through Cayman Islands accounts. Other subsidiaries moved money from Iran, Syria and other countries on US sanctions lists and helped a Saudi bank linked to al-Qaida to shift money to the US. [4] [5]

Fearful of the damage that prosecuting HSBC for money laundering might do to one of the world’s largest banks, state and federal agencies agreed to allow a $1.92 billion settlement and HSBC agreed to hire an independent monitor to evaluate its progress in improving its compliance. Along with the fine, CEO Stuart Gulliver stated: “We accept responsibility for our past mistakes. We have said we are profoundly sorry for them, and we do so again. The HSBC of today is a fundamentally different organization from the one that made those mistakes.” [6]

Lord Green, the CEO of HSBC during the time of the investigations, is now the British Trade Minister after having stepped down in 2010. Green has stated that he “regrets” the money laundering HSBC did while he was at the helm. [7]

Carl Levin, who led the US Senate investigation of the bank stated: “The HSBC settlement sends a powerful wake-up call to multinational banks about the consequences of disregarding their anti-money laundering obligations.” [4]

One has to wonder who Levin thinks he is fooling. HSBC laundered over $670 Billion in Mexican drug cartel money alone. The profits from just those transactions would dwarf the $1.92 billion settlement they paid. Ultimately, the prosecutor’s office came to believe the case was “the tip of the iceberg” in terms of suspicious transactions conducted through HSBC. Not only this, but HSBC was also caught money laundering in 2003 and 2010. But this time they’re “sorry?” The settlement removes any fear of prosecution for the employees of HSBC. As Analyst Jim Antos of Mizuho Securities said, the settlement costs were “trivial” in terms of the company’s book value. So a “too-big-to-fail” bank gets a slap on the wrist and is sent on its way to launder some more money. [4]

Another point to ponder is where were the regulators we rely on to catch crooks like this? Senate Permanent Investigations Subcommittee reported that “the Office of the Comptroller of the Currency (which is the nation’s primary bank overseer) — “had failed to take a single enforcement action against the bank, formal or informal, over the previous six years, despite ample evidence” of money laundering. [8]

The Evil Empire

There are many companies in America today deserving the title of “the Evil Empire,” and for many reasons. Monsanto with Agent Orange, [9] GMO seeds, [10] and PCBs [11]; Union Carbide with Bhopal, India [12]; and Pfizer and the false claims with Bextra and other drugs as well as the bogus patent dispute over Norvasc [13] [14] all certainly deserve this title for the amount of destruction they have visited on their victims. Proudly joining their fellow low-life corporations in the race, a serious argument can be made for Bank of America to own that title outright.

Bank of America was started in 1904 by a first-generation Italian-American named Amadeo Giannini in San Francisco and originally set out to serve immigrants denied credit by other banks. It played an important part in helping the city to rebuild after the devastating 1906 earthquake. Over the years, however, it has grown into the second-largest bank holding company in the United States, the third-largest non-oil company in the U.S. and is the third biggest company in the world. The company held 12.2% of all bank deposits in the United States as of August 2009 and has financial dealings with approximately 80 percent of the U.S. population. With all this wealth and power, one might wonder why they need to resort to stealing to get even more. [15]

But like the meth addict who can think only of his next high, Bank of America lives to steal, lie and dodge responsibility, but unlike the normal Joe meth addict, B of A has the blessings of the government to continue on in its illicit gains.

The 2008 housing bust that vaporized trillions of dollars of investments can be summarized by saying that banks and mortgage lenders, working in concert, created millions of loans to people who had no ability to pay them back. Then the banks falsified the information on the people taking out the loans through bogus math and creative accounting and turned these bad home loans into AAA-rated securities that were sold off to unions, pensioners, foreign banks, retirement accounts and anyone else they could find. Like the fabled alchemists of the medieval age, these bankers had turned straw into gold for themselves at the expense of millions of innocent victims. [16] [17]

B of A perfected its sales pitch for these toxic debts by claiming these mortgages had met extremely high internal standards. They also promised to buy back any of the loans that turned sour and as a further guarantee of the loans’ security, said the loans were insured by bond insures like AMBAC and MBIA. Unfortunately, the buyers should have remembered the rule of thumb that if something seems too good to be true, it generally is. They are at least partially responsible for their own fleecing. [16]

Many of these loans unraveled almost instantly, but when the purchasers tried to get B of A to buy them back, they were met by stonewalling and unanswered phone calls. So in desperation, many of the purchasers turned these toxic loans over to the insurance companies B of A had contracted with to cover them. This only drove many of the insurers out of business, leaving millions of bad loans worth billions of dollars in the hands of now-desperate investors losing money by the day. [16] [17]

In 2011, the bank settled with a group of pension and retirement funds that charged Bank of America with misrepresenting the value of more than $16 billion in mortgage-backed securities. B of A was fined a measly $315 million. They paid out $2.7 billion to settle claims brought by defrauded customers. [16] [17]

Manal Mehta, a partner at the hedge fund Branch Hill Capital, spent two years studying the fraud Bank of America pulled on investors and had this to say of it: “It’s one of the biggest reverse transfers of wealth in history – from pensioners to financiers.” What the 99 percent should understand is that Wall Street knowingly inflated the bubble by engaging in rampant mortgage fraud – and then profited from the collapse of their own exuberance by devising a way to shift the losses to countless pension funds, endowments and other innocent investors.” [16] [17]

B of A realized they could rip off counties all over the country by simply not filing the needed paperwork on the mortgages they were creating and selling. Along with many other banks, it created a system called the Mortgage Electronic Registration System, or MERS, which enabled the financial institutions to avoid some $2 billion in county recording fees. Around 70 million mortgage loans are in the MERS system which forces counties to raise property taxes to compensate for the lost revenue. [19]

One thing that Bank of America has to be credited with, however, is creativity; they are ingenious at finding ways to rip people off. Because the MERS system failed to produce the needed documents to throw people out of their homes when the loans started to fail, it had no evidence to take to court. So Bank of America created a practice called robo-signing, which essentially involved drawing up fake documents for court procedures. They produced these document packages by the hundreds or even thousands every day with the blessing of management. In November of 2012, they were fined $15.8 billion for this practice, which is a pittance in comparison to the profits they made and the number of people they illegally tossed from their homes. They were also caught still doing it in 2012 after promising to stop. [18]

B of A has stolen from their depositors by way of bogus bank charges to the tune of $4.5 billion. When caught and convicted of this, they were forced to repay their depositors a mere $450 million. They also have no problem with lying to their investors as they did when acquiring Merrill Lynch in 2009. When announcing the purchase of Merrill Lynch, the B of A executives understated the amount of debt Merrill Lynch had by many millions of dollars. Once caught, Bank of America agreed to pay US $62.5 million as part of a larger $2.4 billion lawsuit over the purchase by investors. [16] [17]

With the purchase of Countrywide Mortgage and Merrill Lynch and all of the lawsuits attached to them in 2008, B of A should have gone out of business. But as in the case of many a well-connected corporation, the federal government was there to bail them out. First, there was $20 billion to help in buying Merrill Lynch, and then there was the $20 billion in the TARP bailout and the government guarantee to cover $118 billion in B of A loans. At least these figures were the ones reported to the public. [16] [17]

Bloomberg.com fought for two years through the Freedom of Information Act to get documents relating to the mortgage crisis of 2008, and what they found was staggering. Since 2008, B of A has been able to issue $44 billion in FDIC-insured debt through a program that allows bankrupt companies to issue loans using taxpayer-backed moneys. That means that when you take out a credit card or a mortgage or a refinancing from Bank of America, you’re essentially borrowing from the state; B of A is simply taking a cut as a middleman. “For banks, the cost of capital is the key to success,” says former New York Governor Eliot Spitzer. “So by lowering their cost of capital to almost zero, the Fed has almost guaranteed that the banks will make big profits.” On one day in 2008, B of A actually owed the Fed $86 billion. [16] [17]

So what did the bank do with that money they borrowed? First, they sat by while lame-duck executives at Merrill paid themselves $3.6 billion in bonuses – even though Merrill lost more than $27 billion that year. In all, 696 executives received more than $1 million each for helping to crash the storied firm. (The bank wound up hit with a $150 million fine for its failure to inform shareholders about the Merrill losses and bonuses.) Bank of America, meanwhile, paid out more than $3.3 billion in bonuses to itself, including more than $1 million each to 172 executives. [16] [17]

It gets worse. Last fall, some of the bank’s biggest creditors and counterparties started to get nervous about the mountain of toxic bets still sitting on Merrill Lynch’s books. Nobody felt good lending Bank of America money with those dangerous debts still on the books. So they asked the bank to move a chunk of that mess from Merrill Lynch onto Bank of America’s own balance sheet. Why? Because Bank of America is a federally-insured depository institution and Merrill Lynch is not. This means that the FDIC is now on the hook for some $55 trillion in potential losses. William Black, a former regulator, calls the transfer an “obscenity. As a regulator, I would have never allowed it. Transferring risk to the insured institution crosses the reddest of red lines.” But that is just another example of the US Government shielding irresponsible businesses and sticking it to the taxpayers. This brings us to LIBOR, which besides the creation of the Federal Reserve in 1913, is the biggest bank scandal of all time. [20]

Last year, B of A was sued, alongside some of its competitors, for conspiring to rig the London Interbank Offered Rate. Many adjustable-rate financial products are based on LIBOR – so if the big banks could get together and artificially lower the rate, they would pay out less to customers who bought those products. “About $350 trillion worth of financial products globally reference LIBOR,” says one antitrust lawyer familiar with the case. “Which means,” she adds in a striking understatement, “that the scale of this conspiracy is extremely large.” [16] [17]

Banks like B of A are not only a threat to our national security but to the world’s financial system as well. Investors and depositors expect their money to be safe when in the hands of banking institutions, but it clearly is not anymore. Banks regularly manipulate and cheat for a profit with little risk of prison time for those making the decisions to operate in unethical ways, having to pay back only a small percentage of the profits they made from the thefts. Their behavior is further rewarded by being covered by taxpayers when the scam comes home to roost. Unfortunately, these banks have created a monster that all the taxpayers in the world could cover: derivatives. [21]

Warren Buffett once said that derivatives are “financial weapons of mass destruction,” and that statement is truer today than it ever has been before. Nine US banks have created over $200 trillion in exposure to derivatives. That is nearly three times the world’s entire economy. It is obvious that the US politicians believe the US taxpayer is the world’s biggest insurance policy, but this, along with our own national debt of $16 trillion and over $100 trillion in unfunded liabilities, puts us at risk of a financial collapse like the world has never seen before. This news is certainly known by President Obama and his staff, yet they do nothing about it but contemplate nationalizing all the 401(k)’s and IRAs out there as a new source of revenue. [21]

In closing, our financial system is in the hands of corrupt and self-serving people who have no concern for the average person. These people have put our planet’s economy at risk for gain and our leaders are still willing to bail them out. There may well come a time when this house of cards collapses and the Great Depression of 1929 will seem like the good old days. Are you prepared for it? Do you still have money in 401(k)s and IRAs that can be stolen without warning? How much are you willing to gamble that the same people capable of grand thefts like those listed about are really looking out for your best interest? It might just be time to pull your money out while you can and invest in things you can actually control. Or you can be like those poor soldiers herded onto the Sultana like sardines in a can, only to find out just how much the government is looking out for you.

- http://thisweekinthecivilwar.com/?p=311/

- http://news.nationalgeographic.com/news/2001/05/0501_river5.html

- http://jgburdette.wordpress.com/2012/03/15/theres-people-in-the-river/

- http://www.nbcnews.com/business/banking-giant-hsbc-pay-record-1-9-billion-money-laundering-1C7541128

- http://www.guardian.co.uk/business/2012/jul/17/hsbc-executive-resigns-senate

- http://dealbook.nytimes.com/2012/12/10/hsbc-said-to-near-1-9-billion-settlement-over-money-laundering/

- http://www.guardian.co.uk/business/2012/jul/24/lord-green-hsbc-scandal

- http://www.nytimes.com/2012/07/21/opinion/nocera-financial-scandal-scorecard.html?_r=3&ref=opinion&

- http://www.guardian.co.uk/environment/2012/feb/24/monsanto-agent-orange-west-virginia

- http://www.globalresearch.ca/killer-seeds-the-devastating-impacts-of-monsanto-s-genetically-modified-seeds-in-india/28629

- http://www.chemicalindustryarchives.org/dirtysecrets/annistonindepth/toxicity.asp

- http://www.khalnayak.in/2011/12/bhopal-wrost-indrustrial-disaster-of.html

- http://articles.latimes.com/2009/sep/03/business/fi-pfizer3

- http://www.naturalnews.com/037123_pfizer_patents_jamaica.html

- http://en.wikipedia.org/wiki/Bank_of_America

- http://www.rollingstone.com/politics/news/bank-of-america-too-crooked-to-fail-20120314?page=2

- http://fthebanks.org/matt-taibbi-on-bank-of-america/

- http://topics.nytimes.com/top/news/business/companies/mortgage_electronic_registration_systems_inc/index.html

- http://dealbook.nytimes.com/2012/10/24/federal-prosecutors-sue-bank-of-america-over-mortgage-program/

- http://www.taipeitimes.com/News/biz/archives/2013/01/13/2003552385

- http://theeconomiccollapseblog.com/archives/when-the-derivatives-market-crashes-and-it-will-u-s-taxpayers-will-be-on-the-hook

There’s not a bookie to be found that will take the bet on the Federal Reserve’s renewed charter that comes due this December: it’s as good as done.

Not one.

The fix has been in for over 100 years, and still the American citizen doesn’t have a clue how they’ve been had, and continue to be taken advantage of by the PRIVATE CORPORATION THAT IS THE FEDERAL RESERVE BANK.

Had I been elected President, all of the Fed’s officers would be in prison for Grand Theft on a grand scale.

Period.

OPOVV